Dying EV Batteries Power a Circular Economy

China has unveiled the world’s first zero-carbon building that combines solar power, retired electric vehicle (EV) batteries, and cutting-edge digital technologies. This innovation not only...

Executive summary

The global grid-scale battery storage system (BESS) market is entering a rapid growth phase: projected to reach 205 GWh installed capacity by end-2025 — roughly 50% growth from the prior year. This acceleration is concentrated in a few regions driven by tariff effects, capacity market reforms, subsidy programs and major announced projects. The United States, Europe, the Middle East and Australia account for the lion’s share of near-term additions; other regions will fill the remainder to meet the 205 GWh global projection.

Key figures (from aggregated securities reports and national sources)

What’s Driving Growth Regionally?

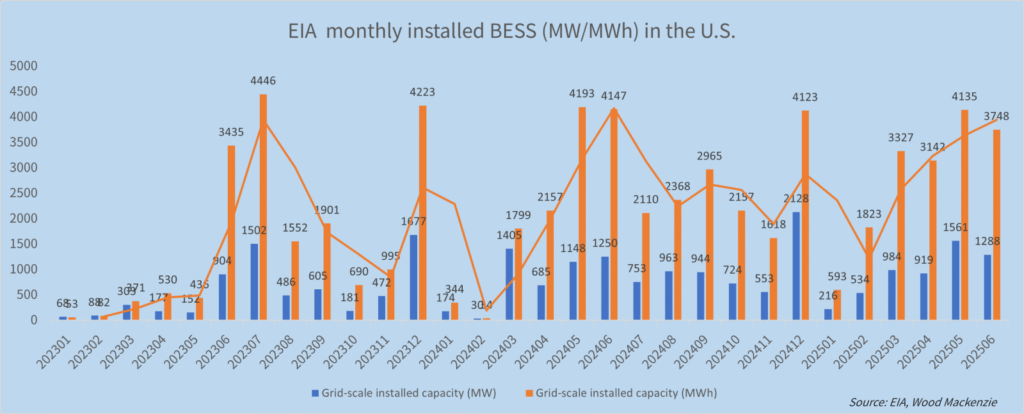

United States — tariffs and market signals

Tariff policy and capacity market structures accelerated deployments in H1 2025, producing a jump in installed capacity (17 GWh in Jan–Jun). The expected end-2025 total of 40 GWh reflects continued utility procurements and merchant project development supported by favorable market prices for capacity and ancillary services.

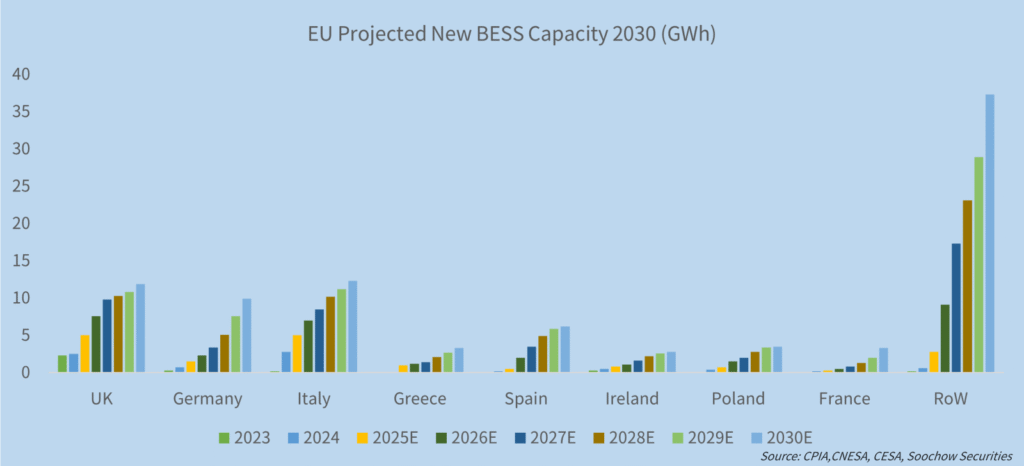

Europe — subsidy programs and auctions

Europe’s 2025 additions are concentrated among several markets and policy initiatives:

Policy landscape across EU member states is supportive: new national aid packages, dedicated storage funds, and targeted subsidies in Spain, Netherlands, Italy and Poland are reducing project risk and improving bankability.

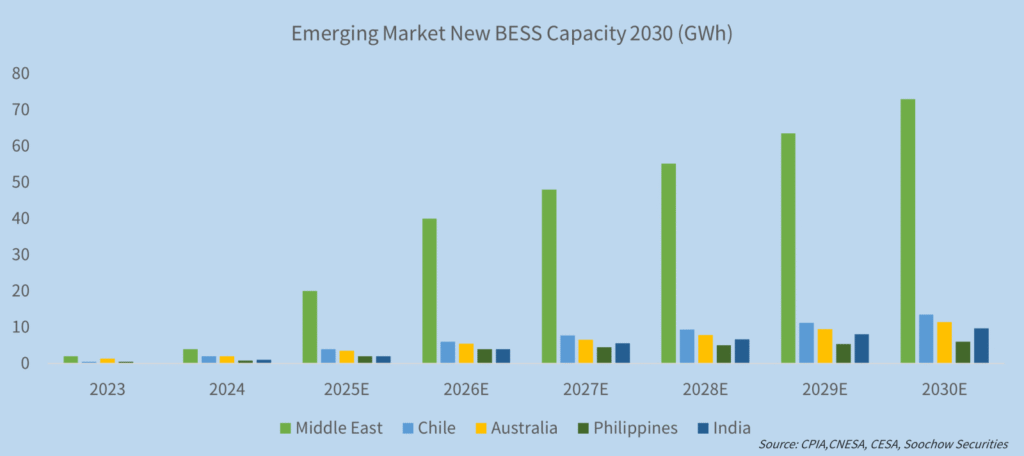

Middle East — utility scale project awards and large signed deals

The region shows a small base but very rapid growth — several multi-hundred-MWh to GWh-scale projects were signed in Saudi Arabia, UAE and Egypt. The projection of 34 GWh in 2025 (≈221% YoY) reflects both early-stage project awards and announced state and utility procurements.

Australia — steady approvals feeding steady growth

Australia’s 1.6 GWh added in 2024 and the 40% growth expectation for 2025–2026 are driven by utility scale projects approved alongside renewables and by demand for grid stability services at the distribution scale.

Interpreting the numbers — where the 205 GWh comes from

Aggregating the verified/regional projections (US 40, Europe 17.6, Middle East 34, Australia ~2.24 and other regions) yields the 205 GWh global projection. Notably, a portion of the global total comes from large projects currently in permitting/approval — as the EU and Middle East auction winners and signed contracts move toward construction, the 2025 commissioning pipeline will swell.

Market dynamics & implications