Grid-Scale Battery Storage in 2025: Market Growth, Regional Trends & Investment Outlook

Executive Summary

The global grid-scale battery energy storage system (BESS) market is entering a rapid growth phase, projected to reach 205 GWh of installed capacity by end-2025 — roughly 50% growth year-on-year. This acceleration is concentrated in a handful of regions, driven by tariff policy, capacity market reforms, subsidy programs, and major project announcements. The United States, Europe, the Middle East, and Australia account for the lion’s share of near-term additions, with other regions contributing the remainder toward the 205 GWh global target.

Key Figures Global and regional installed capacity projections for 2025, based on aggregated securities reports and national sources:

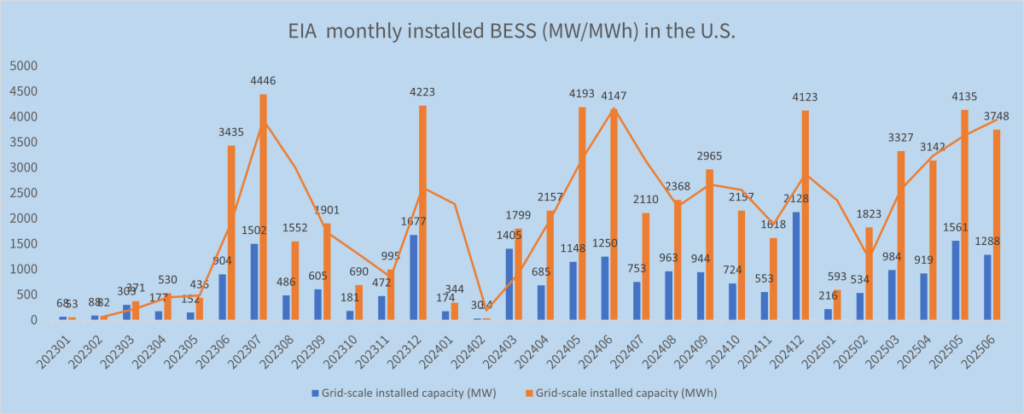

Global grid-scale BESS installed capacity: 205 GWh by end-2025 (+50% YoY) United States: 17 GWh added in H1 2025 (+32% YoY); 40 GWh expected by year-end (+41% YoY) Europe: 17.6 GWh projected additions in 2025 (+120% YoY) Middle East: ~4 GWh newly added; total expected to reach 34 GWh in 2025 (+221% YoY), with major deals in Saudi Arabia, UAE, and Egypt Australia: 1.6 GWh added in 2024; projected ~40% growth in 2025 (~2.24 GWh)

What’s Driving Growth — A Regional Breakdown United States: Tariffs and Capacity Market Signals Tariff policy and capacity market structures accelerated deployments in H1 2025, with 17 GWh installed in the first six months alone. The projected year-end total of 40 GWh reflects continued utility procurement and merchant project development, supported by favourable pricing for capacity and ancillary services.

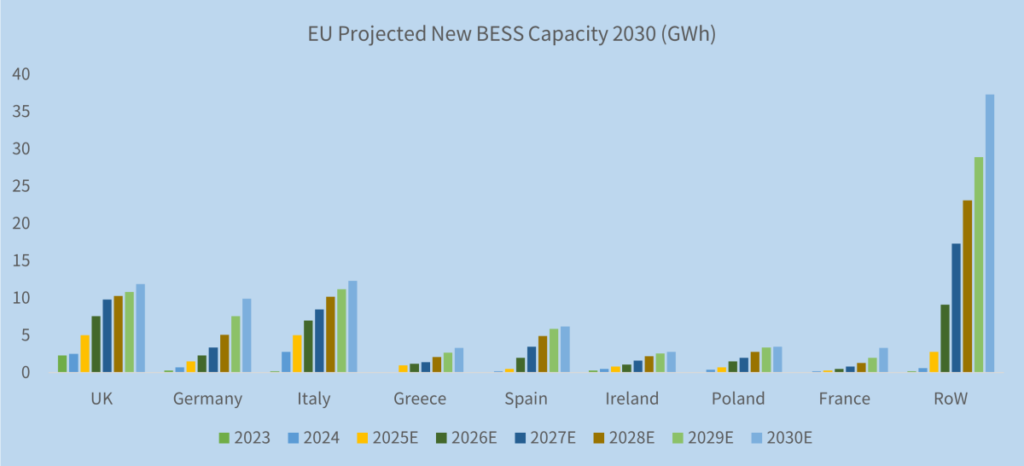

Europe: Subsidy Programs and Competitive Auctions Europe’s 2025 additions are spread across several markets, each with distinct policy drivers:

UK — Operational BESS reached 9.2 GWh in May 2025, with H1 2025 showing +20% YoY growth in commissioned capacity. The near-term pipeline remains strong, with 7.489 GWh submitted for approval as of June 2025. Italy — Connected storage reached 5.9 GWh in 2024 (+41% YoY), with 1.3 GWh added in Q4 alone. The MACSE auction mechanism is introducing competition and scale, with early auction awards adding large blocks of new capacity. Germany — Policy reforms reintroduced stronger investment subsidies and broadened capacity market access. Large-scale additions totalled 0.73 GWh in 2024, followed by 0.716 GWh in just the first seven months of 2025.

Across the EU more broadly, national aid packages, dedicated storage funds, and targeted subsidies in Spain, the Netherlands, Italy, and Poland are reducing project risk and improving bankability.

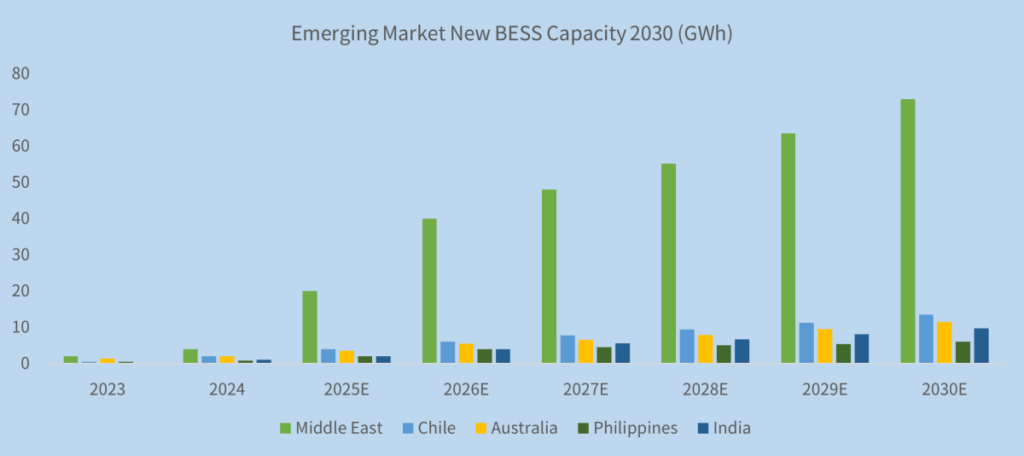

Middle East: Utility-Scale Awards and State Procurement

Starting from a relatively small base, the Middle East is growing at exceptional speed. Several multi-hundred-MWh to GWh-scale projects have been signed in Saudi Arabia, the UAE, and Egypt. The projected total of 34 GWh in 2025 — a 221% YoY increase — reflects a combination of early-stage project awards and state and utility-led procurement programs.

Australia: Steady Approvals, Steady Growth

Australia’s growth is more measured but consistent. The 1.6 GWh added in 2024 and the 40% growth expected through 2025–2026 are being driven by utility-scale projects approved alongside renewables and by rising demand for grid stability services at the distribution level.

Where Does the 205 GWh Global Figure Come From?

Aggregating verified regional projections — the US (40 GWh), Europe (17.6 GWh), Middle East (34 GWh), Australia (~2.24 GWh), and other regions — yields the 205 GWh global estimate. A meaningful portion of this total depends on projects currently in permitting or approval; as EU and Middle East auction winners move toward construction, the 2025 commissioning pipeline is set to grow further.

Market Dynamics and Implications

1. Supply Chain and Procurement Pressure

Rapid growth in concentrated markets — particularly the US and Middle East — will strain cell supply and module assembly capacity. Suppliers with robust manufacturing footprints or secured long-term cell contracts will be best positioned to fulfil 2025 order books.

2. Contracting and Pricing Volatility

Competitive auctions and capacity market price signals are compressing developer returns, with some auction results coming in well below reserve premiums. To protect margins, developers will need to optimise capital and operating costs, and consider hybrid strategies such as PPAs or aggregator-based revenue stacking.

3. Technology Mix and Storage Duration

Most recent capacity additions are short-duration systems (1–2 hours) designed for capacity and frequency markets. However, a shift is underway: national programs and auction frameworks are increasingly favouring longer-duration systems (2+ hours). Germany’s subsidy structure, for example, prioritises 2+ hour systems, improving the economics for larger energy capacity installations.

4. Geopolitical and Policy Risk

State-backed subsidy schemes and infrastructure funds reduce individual project risk, but they also concentrate exposure to policy shifts. Developers relying on a single national scheme should build in contingency for regulatory changes or funding delays.